Share this article

Trade tensions between the United States and China have escalated in recent weeks, with both countries implementing unprecedented tariff increases. For the moment, the U.S. has raised tariffs on Chinese goods to 145%, while China has countered with 125% tariffs on American products. The situation is evolving quickly and continues to affect financial markets. While global tensions can create uncertainty, history shows that markets have weathered similar challenges in the past. Despite the headlines, understanding the economic relationship between these two countries can help long-term investors to maintain perspective.

U.S.-China Trade Tensions Are Now in Focus

Tariffs against all trading partners have dominated market news, and the 90-day pause now puts the focus on the U.S.-China relationship. The underlying issue runs much deeper than trade policy alone. Current tensions are a result of the “multipolar” world in which the U.S. and China are the two largest economies, both with significant global influence. This is a decades-long shift from the “unipolar” world in which the U.S. was the only major superpower after the Cold War. This naturally creates new challenges and opportunities for each country.

While there are no easy answers as to how the trade war might progress over the next few months, maintaining perspective has become even more important for long-term investors. The U.S. and China remain significantly linked through trade, finance, and global supply chains.

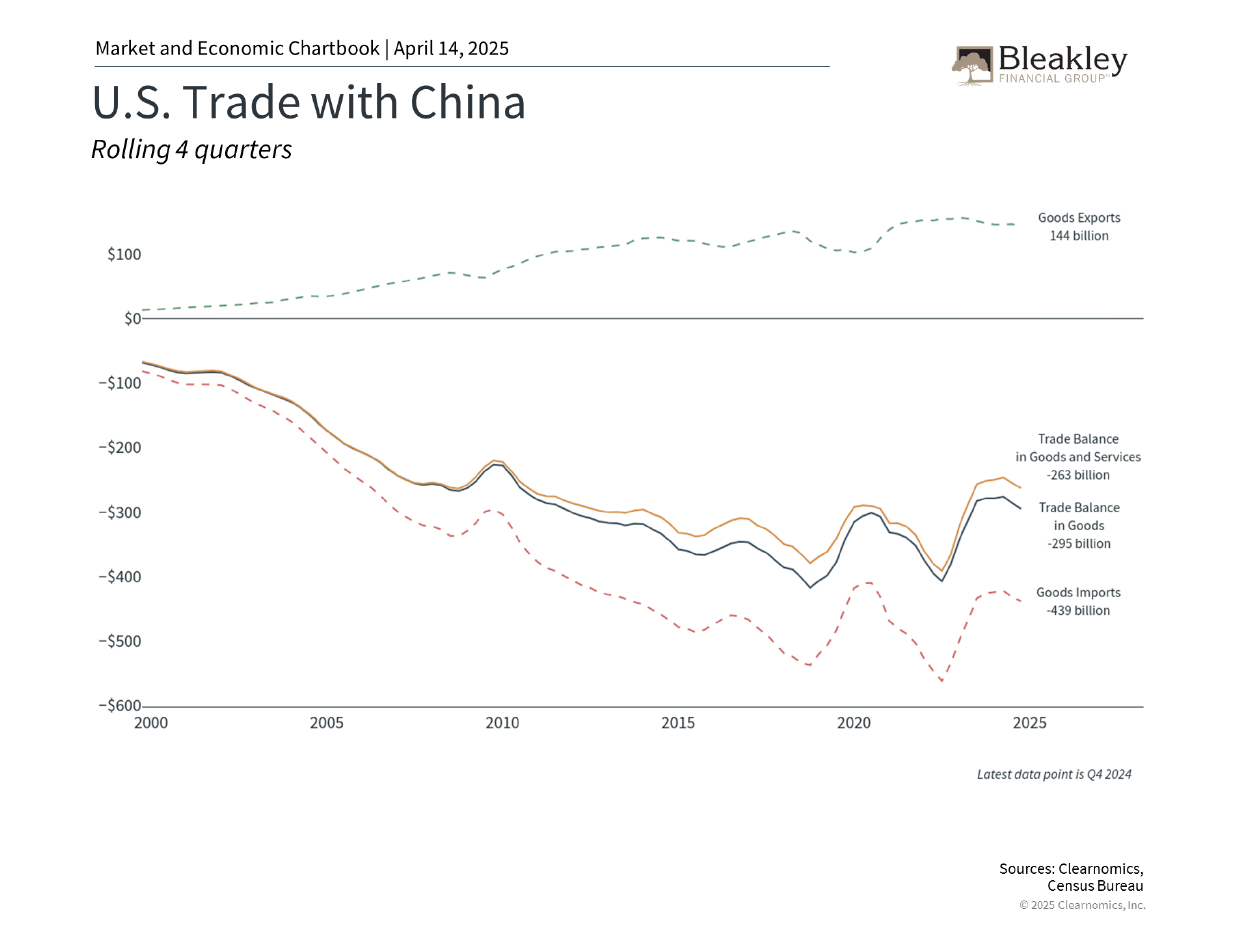

What makes this situation different from previous trade tensions is both the magnitude of the tariffs and the broader geopolitical context. As the accompanying chart shows, the U.S. maintains a significant trade deficit with China. Tariff levels above 100% effectively mean that goods crossing either border would more than double in price, all else being equal. This increases the price of goods for consumers, raises costs for businesses, and can slow economic activity. The fear of high inflation and worsening profit margins has caused market volatility in recent weeks, with a notable shift in consumer surveys and corporate earnings guidance.

Markets have also been worried about how far the White House would be willing to go in escalating a trade war with China. Since tariffs at these levels are unlikely to be sustainable in the long run, it’s still likely that they represent a negotiating position for the administration. The 90-day pause on tariffs above 10% (except for China), and the exemption for technology products, are evidence that the White House’s main objective is still to achieve deals.

The tariffs implemented in 2018 and 2019 provide some historical context for how markets and companies might respond as the situation evolves. Many companies demonstrated resilience by adjusting supply chains, finding alternative suppliers, or absorbing portions of the increased costs. While markets stumbled in 2018, they performed well in 2019 and again during the post-pandemic recovery. The broader scope of tariffs makes it more difficult for companies this time around, but the historic market rally after the 90-day pause was announced is evidence that markets can recover once conditions improve.

For investors with long-term horizons, this challenging market environment can create opportunities. Valuations are much more attractive than they were even just a few months ago, both across the broad market and in sectors like Information Technology and Communication Services that drove the recent bull market. Rising interest rates have led to bond market volatility, but they also mean that investors have more opportunities to generate portfolio income.

China’s Economy Faces Many Challenges

While much attention has focused on the U.S. response to trade tensions, China faces its own set of economic challenges. These include persistent concerns of a real estate bubble and financial system instability that could impact its ability to withstand trade tensions. China's post-pandemic recovery has been uneven, with GDP growth slowing to 5.4% year-over-year in late 2024, according to official Chinese government statistics. Many economists have already reduced their 2025 growth forecasts below the government's 5% target.

Chinese leaders are reportedly considering more stimulus measures. This would be on top of significant stimulus measures implemented last year, including a 5-year, 10 trillion-yuan stimulus package to support local government debt issues, a commitment to increase the budget deficit, cut interest rates, reduce bank reserve requirements, and measures to support the real estate market.

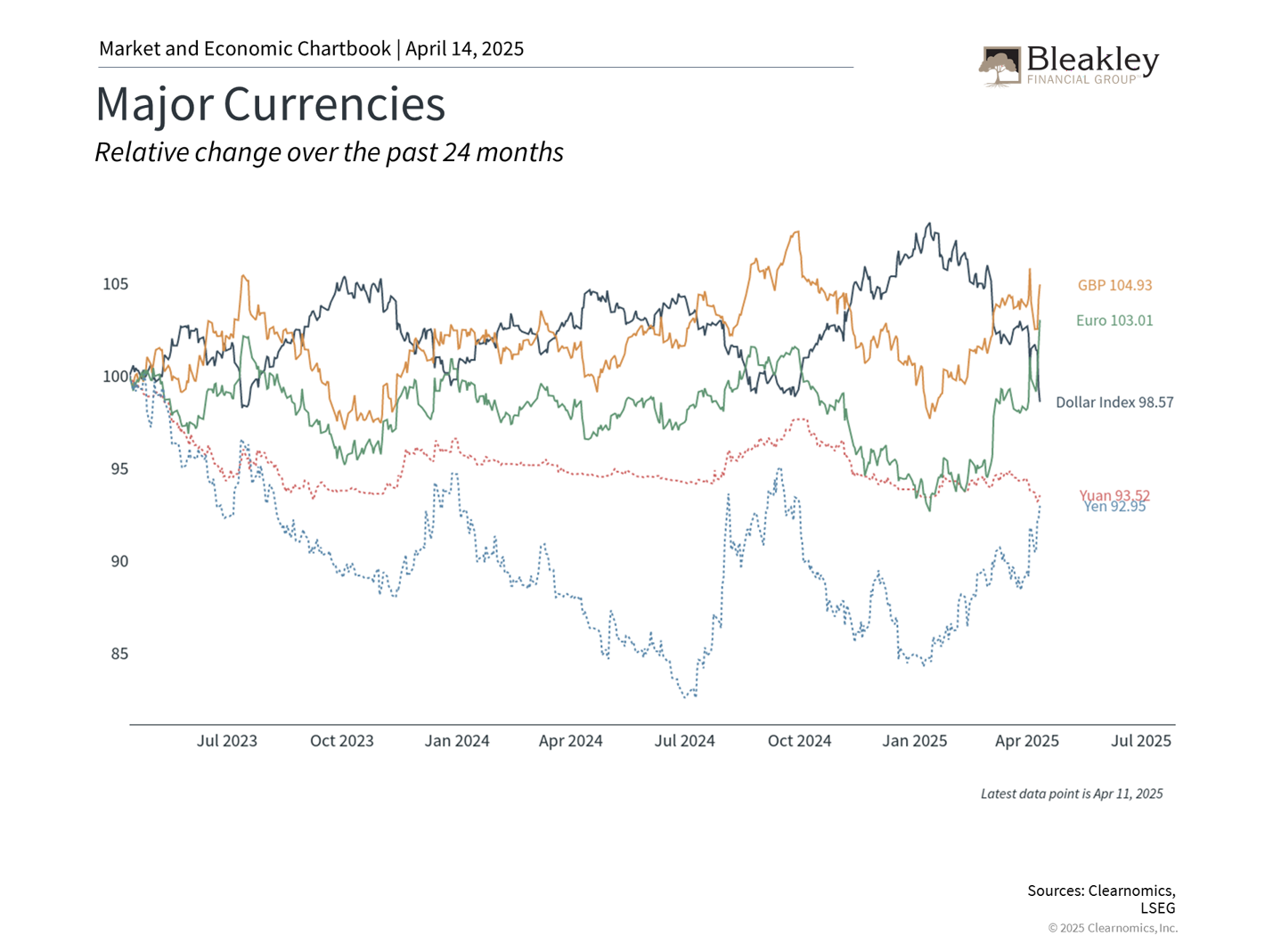

In recent days, the People's Bank of China has also allowed the yuan to weaken as a potential offset to tariff impacts, including setting its currency peg to the weakest level since September 2023. Currency devaluation can help boost exports by making goods cheaper for foreign buyers. However, it also carries risks including capital outflows, which is especially risky for China since it could destabilize its financial system further. It can also be seen by the White House as an attempt to circumvent tariffs.

The chart above, which shows major currencies indexed to a level of 100 two years ago, highlights how volatile global currencies have been in recent weeks. In addition to the yuan’s moves, the value of the U.S. dollar index has fallen to the low end of the range over the past three years. This is the opposite of what some expected since, in theory, tariffs tend to reduce imports, lowering the need for foreign currency, and thus boosting the value of the dollar.

Most U.S. Debt Is Held Domestically

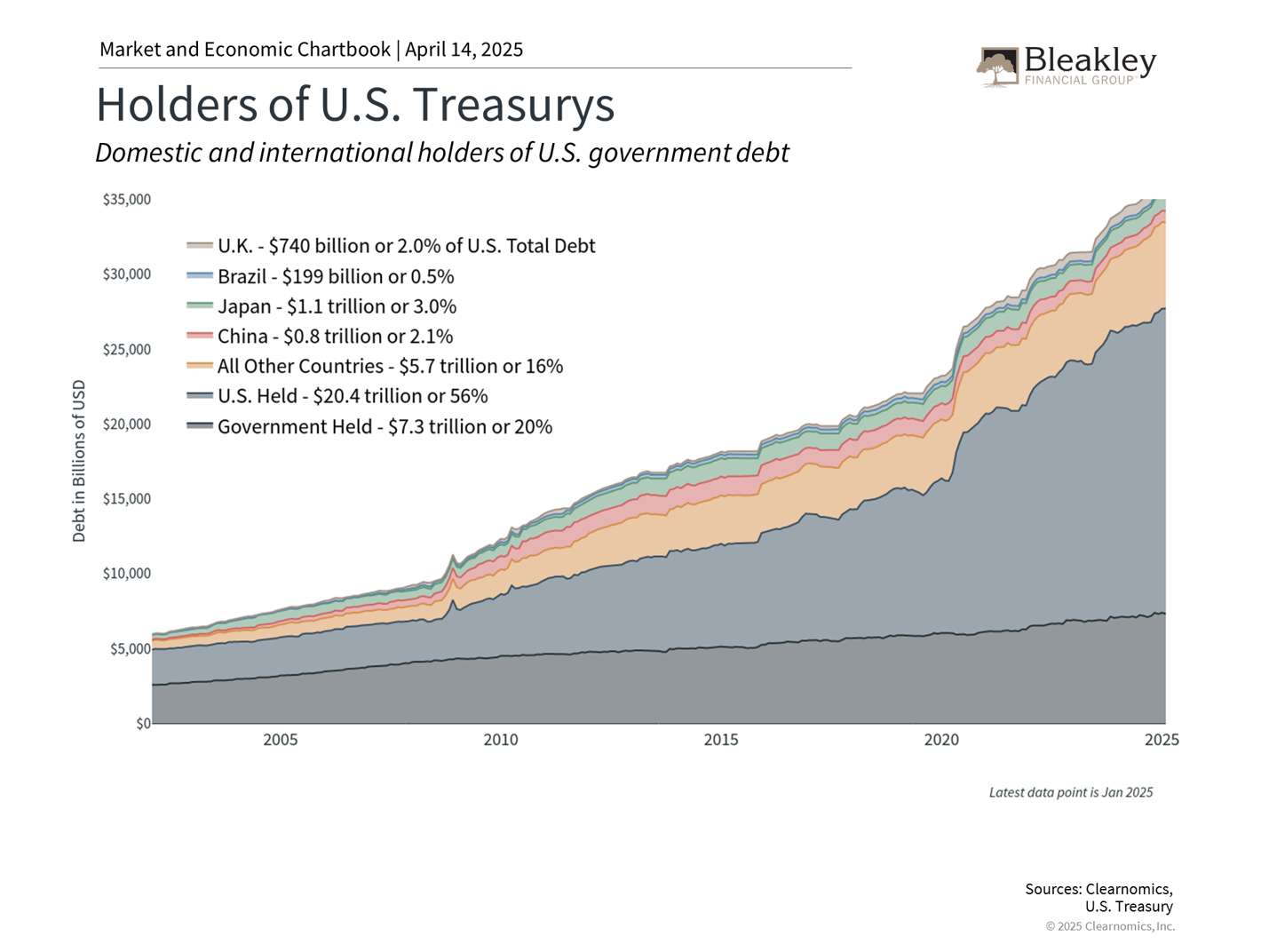

Some investors also worry that China's holdings of U.S. Treasury securities give them undue influence over the U.S. economy. There have been concerns that recent moves in the bond market are the result of countries like China selling their U.S. Treasuries. While this is difficult to verify, what’s clear is that China's Treasury holdings represent about 2.1% of total U.S. government debt according to government data. Importantly, most Treasury securities are still held domestically by U.S. individuals, corporations, and other federal, state, and local government entities.

If China were to significantly reduce its Treasury holdings, it could potentially cause short-term market volatility and temporarily push up U.S. interest rates. However, China and other countries hold U.S. Treasuries, the dollar, and other foreign assets for an important reason: to maintain financial stability. The U.S. dollar and Treasury securities have consistently maintained their "safe haven" status even during periods of uncertainty. This has been true over the past few years despite inflation fears, budget crises, U.S. debt downgrades, and more.

The bottom line? While escalating U.S.-China trade tensions create uncertainty, history shows that financial markets are resilient in the long run. A diversified portfolio aligned with your long-term financial goals remains the best approach to navigating the changing global landscape.

- Article published on 4/14/25 -

BFG 25-0062

Disclaimer

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. The market and economic data is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The information in this report has been prepared from data believed to be reliable, but no representation is being made as to its accuracy and completeness.

This commentary is for informational purposes only and is not meant to constitute a recommendation of any particular investment, security, portfolio of securities, transaction or investment strategy. No chart, graph, or other figure provided should be used to determine which securities to buy, sell or hold. No representation is made concerning the appropriateness of any particular investment, security, portfolio of securities, transaction or investment strategy. You should speak with your own financial professional before making any investment decisions.

Past performance is not indicative of future results. Bleakley Financial Group, LLC does not guarantee any specific outcome or profit. These disclosures cannot and do not list every conceivable factor that may affect the results of any investment or investment strategy. Risks will arise, and an investor must be willing and able to accept those risks, including the loss of principal.

Certain statements contained herein are statements of future expectations and other forward-looking statements that are based on opinions and assumptions that involve known and unknown risks and uncertainties that would cause actual results, performance or events to differ materially from those expressed or implied in such statements.

The economic forecasts set forth in this material may not develop as predicted and there can be no guarantee that strategies promoted will be successful. The fast price swings in commodities and currencies will result in significant volatility in an investor’s holdings. International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets. The fast price swings in commodities and currencies will result in significant volatility in an investor’s holdings.

Copyright (c) 2025 Clearnomics, Inc. All rights reserved. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.clearnomics.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally, but should not be construed as a recommendation to buy, sell, or hold the company's stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security--including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. The text, images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute valuable intellectual property. All unauthorized reproduction or other use of material from Clearnomics, Inc. shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Clearnomics, Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Clearnomics, Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.

About the Author